![]()

Set-up instructions: this notebook give a tutorial on the forecasting learning task supported by sktime. On binder, this should run out-of-the-box.

To run this notebook as intended, ensure that sktime with basic dependency requirements is installed in your python environment.

To run this notebook with a local development version of sktime, an editable developer installation is recommended, see the sktime developer install guide for instructions.

Forecasting with sktime#

In forecasting, past data is used to make temporal forward predictions of a time series. This is notably different from tabular prediction tasks supported by scikit-learn and similar libraries.

sktime provides a common, scikit-learn-like interface to a variety of classical and ML-style forecasting algorithms, together with tools for building pipelines and composite machine learning models, including temporal tuning schemes, or reductions such as walk-forward application of scikit-learn regressors.

Section 1 provides an overview of common forecasting workflows supported by sktime.

Section 2 discusses the families of forecasters available in sktime.

Section 3 discusses advanced composition patterns, including pipeline building, reduction, tuning, ensembling, and autoML.

Section 4 gives an introduction to how to write custom estimators compliant with the sktime interface.

Further references: * For further details on how forecasting is different from supervised prediction à la scikit-learn, and pitfalls of misdiagnosing forecasting as supervised prediction, have a look at this notebook * For a scientific reference, take a look at our paper on forecasting with sktime in which we discuss sktime’s forecasting module in more detail and use it to replicate and extend the M4 study.

Table of Contents#

1. Basic forecasting workflows

1.1 Data container format

1.2 Basic deployment workflow - batch fitting and forecasting

1.2.1 Basic deployment workflow in a nutshell

1.2.2 Forecasters that require the horizon when fitting

1.2.3 Forecasters that can make use of exogeneous data

1.2.4 Multivariate Forecasters

1.2.5 Prediction intervals and quantile forecasts

1.2.6 Panel forecasts and hierarchical forecasts

1.3 Basic evaluation workflow - evaluating a batch of forecasts against ground truth observations

1.3.1 The basic batch forecast evaluation workflow in a nutshell - function metric interface

1.3.2 The basic batch forecast evaluation workflow in a nutshell - metric class interface

1.4 Advanced deployment workflow: rolling updates & forecasts

1.4.1 Updating a forecaster with the update method

1.4.2 Moving the “now” state without updating the model

1.4.3 Walk-forward predictions on a batch of data

1.5 Advanced evaluation workflow: rolling re-sampling and aggregate errors, rolling back-testing

2. Forecasters in sktime - searching, tags, common families

2.1 Forecaster lookup - the registry

2.2 Forecaster tags

2.2.1 Capability tags: multivariate, probabilistic, hierarchical

2.2.2 Finding and listing forecasters by tag

2.2.3 Listing all forecaster tags

2.3 Common forecaster types

2.3.1 Exponential smoothing, theta forecaster, autoETS from statsmodels

2.3.2 ARIMA and autoARIMA

2.3.3 BATS and TBATS

2.3.4 Facebook prophet

2.3.5 State Space Model (Structural Time Series)

2.3.6 AutoArima from StatsForecast

3. Advanced composition patterns - pipelines, reduction, autoML, and more

3.1 Reduction: from forecasting to regression

3.2 Pipelining, detrending and deseasonalization

3.2.1 The basic forecasting pipeline

3.2.2 The Detrender as pipeline component

3.2.3 Complex pipeline composites and parameter inspection

3.3 Parameter tuning

3.3.1 Basic tuning using ForecastingGridSearchCV

3.3.2 Tuning of complex composites

3.3.3 Selecting the metric and retrieving scores

3.4 autoML aka automated model selection, ensembling and hedging

3.4.1 autoML aka automatic model selection, using tuning plus multiplexer

3.4.2 autoML: selecting transformer combinations via OptimalPassthrough

3.4.3 Simple ensembling strategies

3.4.4 Prediction weighted ensembles and hedge ensembles

4. Extension guide - implementing your own forecaster

5. Summary

Package imports#

[1]:

import warnings

import numpy as np

import pandas as pd

# hide warnings

warnings.filterwarnings("ignore")

1. Basic forecasting workflows#

This section explains the basic forecasting workflows, and key interface points for it.

We cover the following four workflows:

Basic deployment workflow: batch fitting and forecasting

Basic evaluation workflow: evaluating a batch of forecasts against ground truth observations

Advanced deployment workflow: fitting and rolling updates/forecasts

Advanced evaluation workflow: using rolling forecast splits and computing split-wise and aggregate errors, including common back-testing schemes

All workflows make common assumptions on the input data format.

sktime uses pandas for representing time series:

pd.DataFramefor time series and sequences, primarily. Rows represent time indices, columns represent variables.pd.Seriescan also be used for univariate time series and sequencesnumpyarrays (1D and 2D) can also be passed, butpandasuse is encouraged.

The Series.index and DataFrame.index are used for representing the time series or sequence index. sktime supports pandas integer, period and timestamp indices for simple time series.

sktime supports further, additional container formats for panel and hierarchical time series, these are discussed in Section 1.6.

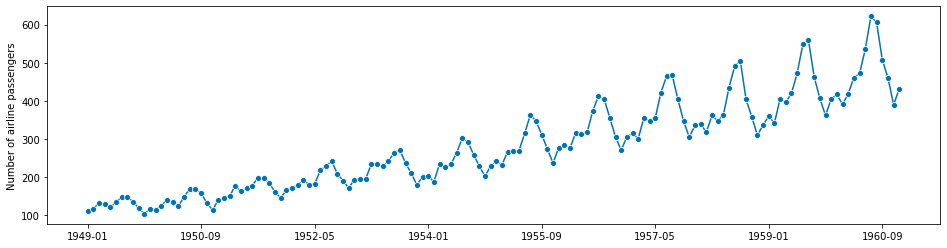

Example: as the running example in this tutorial, we use a textbook data set, the Box-Jenkins airline data set, which consists of the number of monthly totals of international airline passengers, from 1949 - 1960. Values are in thousands. See “Makridakis, Wheelwright and Hyndman (1998) Forecasting: methods and applications”, exercises sections 2 and 3.

[2]:

from sktime.datasets import load_airline

from sktime.utils.plotting import plot_series

[3]:

y = load_airline()

# plotting for visualization

plot_series(y)

[3]:

(<Figure size 1152x288 with 1 Axes>,

<AxesSubplot:ylabel='Number of airline passengers'>)

[4]:

y.index

[4]:

PeriodIndex(['1949-01', '1949-02', '1949-03', '1949-04', '1949-05', '1949-06',

'1949-07', '1949-08', '1949-09', '1949-10',

...

'1960-03', '1960-04', '1960-05', '1960-06', '1960-07', '1960-08',

'1960-09', '1960-10', '1960-11', '1960-12'],

dtype='period[M]', length=144)

Generally, users are expected to use the in-built loading functionality of pandas and pandas-compatible packages to load data sets for forecasting, such as read_csv or the Series or DataFrame constructors if data is available in another in-memory format, e.g., numpy.array.

sktime forecasters may accept input in pandas-adjacent formats, but will produce outputs in, and attempt to coerce inputs to, pandas formats.

NOTE: if your favourite format is not properly converted or coerced, kindly consider to contribute that functionality to sktime.

The simplest use case workflow is batch fitting and forecasting, i.e., fitting a forecasting model to one batch of past data, then asking for forecasts at time point in the future.

The steps in this workflow are as follows:

Preparation of the data

Specification of the time points for which forecasts are requested. This uses a

numpy.arrayor theForecastingHorizonobject.Specification and instantiation of the forecaster. This follows a

scikit-learn-like syntax; forecaster objects follow the familiarscikit-learnBaseEstimatorinterface.Fitting the forecaster to the data, using the forecaster’s

fitmethodMaking a forecast, using the forecaster’s

predictmethod

The below first outlines the vanilla variant of the basic deployment workflow, step-by-step.

At the end, one-cell workflows are provided, with common deviations from the pattern (Sections 1.2.1 and following).

Step 1 - Preparation of the data#

As discussed in Section 1.1, the data is assumed to be in pd.Series or pd.DataFrame format.

[5]:

from sktime.datasets import load_airline

from sktime.utils.plotting import plot_series

[6]:

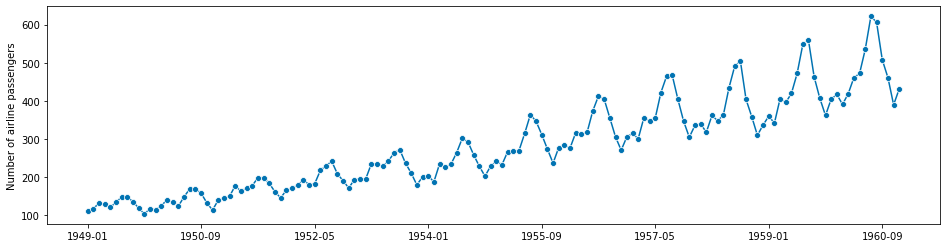

# in the example, we use the airline data set.

y = load_airline()

plot_series(y)

[6]:

(<Figure size 1152x288 with 1 Axes>,

<AxesSubplot:ylabel='Number of airline passengers'>)

Step 2 - Specifying the forecasting horizon#

Now we need to specify the forecasting horizon and pass that to our forecasting algorithm.

There are two main ways:

Using a

numpy.arrayof integers. This assumes either integer index or periodic index (PeriodIndex) in the time series; the integer indicates the number of time points or periods ahead we want to make a forecast for. E.g.,1means forecast the next period,2the second next period, and so on.Using a

ForecastingHorizonobject. This can be used to define forecast horizons, using any supported index type as an argument. No periodic index is assumed.

Forecasting horizons can be absolute, i.e., referencing specific time points in the future, or relative, i.e., referencing time differences to the present. As a default, the present is that latest time point seen in any y passed to the forecaster.

numpy.array based forecasting horizons are always relative; ForecastingHorizon objects can be both relative and absolute. In particular, absolute forecasting horizons can only be specified using ForecastingHorizon.

Using a numpy forecasting horizon#

[7]:

fh = np.arange(1, 37)

fh

[7]:

array([ 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17,

18, 19, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30, 31, 32, 33, 34,

35, 36])

This will ask for monthly predictions for the next three years, since the original series period is 1 month. In another example, to predict only the second and fifth month ahead, one could write:

import numpy as np

fh = np.array([2, 5]) # 2nd and 5th step ahead

Using a ForecastingHorizon based forecasting horizon#

The ForecastingHorizon object takes absolute indices as input, but considers the input absolute or relative depending on the is_relative flag.

ForecastingHorizon will automatically assume a relative horizon if temporal difference types from pandas are passed; if value types from pandas are passed, it will assume an absolute horizon.

To define an absolute ForecastingHorizon in our example:

[8]:

from sktime.forecasting.base import ForecastingHorizon

[9]:

fh = ForecastingHorizon(

pd.PeriodIndex(pd.date_range("1961-01", periods=36, freq="M")), is_relative=False

)

fh

[9]:

ForecastingHorizon(['1961-01', '1961-02', '1961-03', '1961-04', '1961-05', '1961-06',

'1961-07', '1961-08', '1961-09', '1961-10', '1961-11', '1961-12',

'1962-01', '1962-02', '1962-03', '1962-04', '1962-05', '1962-06',

'1962-07', '1962-08', '1962-09', '1962-10', '1962-11', '1962-12',

'1963-01', '1963-02', '1963-03', '1963-04', '1963-05', '1963-06',

'1963-07', '1963-08', '1963-09', '1963-10', '1963-11', '1963-12'],

dtype='period[M]', is_relative=False)

ForecastingHorizon-s can be converted from relative to absolute and back via the to_relative and to_absolute methods. Both of these conversions require a compatible cutoff to be passed:

[10]:

cutoff = pd.Period("1960-12", freq="M")

[11]:

fh.to_relative(cutoff)

[11]:

ForecastingHorizon([ 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17,

18, 19, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30, 31, 32, 33, 34,

35, 36],

dtype='int64', is_relative=True)

[12]:

fh.to_absolute(cutoff)

[12]:

ForecastingHorizon(['1961-01', '1961-02', '1961-03', '1961-04', '1961-05', '1961-06',

'1961-07', '1961-08', '1961-09', '1961-10', '1961-11', '1961-12',

'1962-01', '1962-02', '1962-03', '1962-04', '1962-05', '1962-06',

'1962-07', '1962-08', '1962-09', '1962-10', '1962-11', '1962-12',

'1963-01', '1963-02', '1963-03', '1963-04', '1963-05', '1963-06',

'1963-07', '1963-08', '1963-09', '1963-10', '1963-11', '1963-12'],

dtype='period[M]', is_relative=False)

Step 3 - Specifying the forecasting algorithm#

To make forecasts, a forecasting algorithm needs to be specified. This is done using a scikit-learn-like interface. Most importantly, all sktime forecasters follow the same interface, so the preceding and remaining steps are the same, no matter which forecaster is being chosen.

For this example, we choose the naive forecasting method of predicting the last seen value. More complex specifications are possible, using pipeline and reduction construction syntax; this will be covered later in Section 2.

[13]:

from sktime.forecasting.naive import NaiveForecaster

[14]:

forecaster = NaiveForecaster(strategy="last")

Step 4 - Fitting the forecaster to the seen data#

Now the forecaster needs to be fitted to the seen data:

[15]:

forecaster.fit(y)

[15]:

NaiveForecaster()

Step 5 - Requesting forecasts#

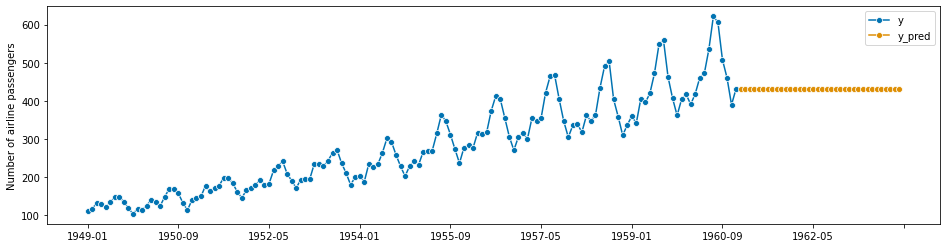

Finally, we request forecasts for the specified forecasting horizon. This needs to be done after fitting the forecaster:

[16]:

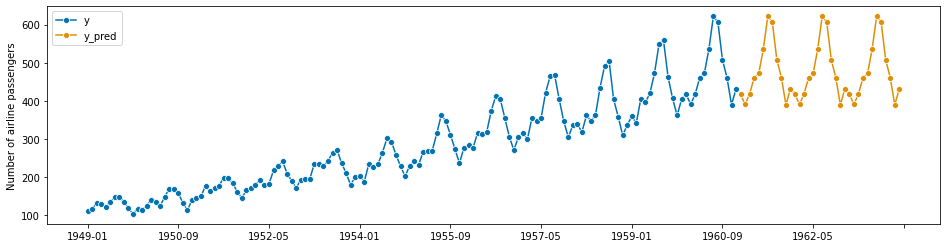

y_pred = forecaster.predict(fh)

[17]:

# plotting predictions and past data

plot_series(y, y_pred, labels=["y", "y_pred"])

[17]:

(<Figure size 1152x288 with 1 Axes>,

<AxesSubplot:ylabel='Number of airline passengers'>)

1.2.1 The basic deployment workflow in a nutshell#

For convenience, we present the basic deployment workflow in one cell. This uses the same data, but different forecaster: predicting the latest value observed in the same month.

[18]:

from sktime.datasets import load_airline

from sktime.forecasting.base import ForecastingHorizon

from sktime.forecasting.naive import NaiveForecaster

[19]:

# step 1: data specification

y = load_airline()

# step 2: specifying forecasting horizon

fh = np.arange(1, 37)

# step 3: specifying the forecasting algorithm

forecaster = NaiveForecaster(strategy="last", sp=12)

# step 4: fitting the forecaster

forecaster.fit(y)

# step 5: querying predictions

y_pred = forecaster.predict(fh)

[20]:

# optional: plotting predictions and past data

plot_series(y, y_pred, labels=["y", "y_pred"])

[20]:

(<Figure size 1152x288 with 1 Axes>,

<AxesSubplot:ylabel='Number of airline passengers'>)

1.2.2 Forecasters that require the horizon already in fit#

Some forecasters need the forecasting horizon provided already in fit. Such forecasters will produce informative error messages when it is not passed in fit. All forecaster will remember the horizon when already passed in fit for prediction. The modified workflow to allow for such forecasters in addition is as follows:

[21]:

# step 1: data specification

y = load_airline()

# step 2: specifying forecasting horizon

fh = np.arange(1, 37)

# step 3: specifying the forecasting algorithm

forecaster = NaiveForecaster(strategy="last", sp=12)

# step 4: fitting the forecaster

forecaster.fit(y, fh=fh)

# step 5: querying predictions

y_pred = forecaster.predict()

1.2.3 Forecasters that can make use of exogeneous data#

Many forecasters can make use of exogeneous time series, i.e., other time series that are not forecast, but are useful for forecasting y. Exogeneous time series are always passed as an X argument, in fit, predict, and other methods (see below). Exogeneous time series should always be passed as pandas.DataFrames. Most forecasters that can deal with exogeneous time series will assume that the time indices of X passed to fit are a super-set of the time indices in y

passed to fit; and that the time indices of X passed to predict are a super-set of time indices in fh, although this is not a general interface restriction. Forecasters that do not make use of exogeneous time series still accept the argument (and do not use it internally).

The general workflow for passing exogeneous data is as follows:

[22]:

# step 1: data specification

y = load_airline()

# we create some dummy exogeneous data

X = pd.DataFrame(index=y.index)

# step 2: specifying forecasting horizon

fh = np.arange(1, 37)

# step 3: specifying the forecasting algorithm

forecaster = NaiveForecaster(strategy="last", sp=12)

# step 4: fitting the forecaster

forecaster.fit(y, X=X, fh=fh)

# step 5: querying predictions

y_pred = forecaster.predict(X=X)

NOTE: as in workflows 1.2.1 and 1.2.2, some forecasters that use exogeneous variables may also require the forecasting horizon only in predict. Such forecasters may also be called with steps 4 and 5 being

forecaster.fit(y, X=X)

y_pred = forecaster.predict(fh=fh, X=X)

1.2.4. Multivariate forecasting#

All forecasters in sktime support multivariate forecasts - some forecasters are “genuine” multivariate, all others “apply by column”.

Below is an example of the general multivariate forecasting workflow, using the VAR (vector auto-regression) forecaster on the Longley dataset from sktime.datasets. The workflow is the same as in the univariate forecasters, but the input has more than one variables (columns).

[23]:

from sktime.datasets import load_longley

from sktime.forecasting.var import VAR

_, y = load_longley()

y = y.drop(columns=["UNEMP", "ARMED", "POP"])

forecaster = VAR()

forecaster.fit(y, fh=[1, 2, 3])

y_pred = forecaster.predict()

The input to the multivariate forecaster y is a pandas.DataFrame where each column is a variable.

[24]:

y

[24]:

| GNPDEFL | GNP | |

|---|---|---|

| Period | ||

| 1947 | 83.0 | 234289.0 |

| 1948 | 88.5 | 259426.0 |

| 1949 | 88.2 | 258054.0 |

| 1950 | 89.5 | 284599.0 |

| 1951 | 96.2 | 328975.0 |

| 1952 | 98.1 | 346999.0 |

| 1953 | 99.0 | 365385.0 |

| 1954 | 100.0 | 363112.0 |

| 1955 | 101.2 | 397469.0 |

| 1956 | 104.6 | 419180.0 |

| 1957 | 108.4 | 442769.0 |

| 1958 | 110.8 | 444546.0 |

| 1959 | 112.6 | 482704.0 |

| 1960 | 114.2 | 502601.0 |

| 1961 | 115.7 | 518173.0 |

| 1962 | 116.9 | 554894.0 |

The result of the multivariate forecaster y_pred is a pandas.DataFrame where columns are the predicted values for each variable. The variables in y_pred are the same as in y, the input to the multivariate forecaster.

[25]:

y_pred

[25]:

| GNPDEFL | GNP | |

|---|---|---|

| 1963 | 121.688295 | 578514.398653 |

| 1964 | 124.353664 | 601873.015890 |

| 1965 | 126.847886 | 625411.588754 |

As said above, all forecasters accept multivariate input and will produce multivariate forecasts. There are two categories:

forecasters that are genuinely multivariate, such as

VAR. Forecasts for one endogeneous (y) variable will depend on values of other variables.forecasters that are univariate, such as

ARIMA. Forecasts will be made by endogeneous (y) variable, and not be affected by other variables.

To display complete list of multivariate forecasters, search for forecasters with 'multivariate' or 'both' tag value for the tag 'scitype:y', as follows:

[26]:

from sktime.registry import all_estimators

for forecaster in all_estimators(filter_tags={"scitype:y": ["multivariate", "both"]}):

print(forecaster[0])

Univariate forecasters have tag value 'univariate', and will fit one model per column. To access the column-wise models, access the forecasters_ parameter, which stores the fitted forecasters in a pandas.DataFrame, fitted forecasters being in the column with the variable for which the forecast is being made:

[27]:

from sktime.datasets import load_longley

from sktime.forecasting.arima import ARIMA

_, y = load_longley()

y = y.drop(columns=["UNEMP", "ARMED", "POP"])

forecaster = ARIMA()

forecaster.fit(y, fh=[1, 2, 3])

forecaster.forecasters_

[27]:

| GNPDEFL | GNP | |

|---|---|---|

| forecasters | ARIMA() | ARIMA() |

1.2.5 Probabilistic forecasting: prediction intervals, quantile, variance, and distributional forecasts#

sktime provides a unified interface to make probabilistic forecasts. The following methods are possibly available for probabilistic forecasts:

predict_intervalproduces interval forecasts. Additionally to anypredictarguments, an argumentcoverage(nominal interval coverage) must be provided.predict_quantilesproduces quantile forecasts. Additionally to anypredictarguments, an argumentalpha(quantile values) must be provided.predict_varproduces variance forecasts. This has same arguments aspredict.predict_probaproduces full distributional forecasts. This has same arguments aspredict.

Not all forecasters are capable of returning probabilistic forecast, but if a forecasters provides one kind of probabilistic forecast, it is also capable of returning the others. The list of forecasters with such capability can be queried by registry.all_estimators, searching for those where the capability:pred_int tag has valueTrue.

The basic workflow for probabilistic forecasts is similar to the basic forecasting workflow, with the difference that instead of predict, one of the probabilistic forecasting methods is used:

[28]:

import numpy as np

from sktime.datasets import load_airline

from sktime.forecasting.theta import ThetaForecaster

# until fit, identical with the simple workflow

y = load_airline()

fh = np.arange(1, 13)

forecaster = ThetaForecaster(sp=12)

forecaster.fit(y, fh=fh)

[28]:

ThetaForecaster(sp=12)

Now we present the different probabilistic forecasting methods.

predict_interval - interval predictions#

predict_interval takes an argument coverage, which is a float (or list of floats), the nominal coverage of the prediction interval(s) queried. predict_interval produces symmetric prediction intervals, for example, a coverage of 0.9 returns a “lower” forecast at quantile 0.5 - coverage/2 = 0.05, and an “upper” forecast at quantile 0.5 + coverage/2 = 0.95.

[29]:

coverage = 0.9

y_pred_ints = forecaster.predict_interval(coverage=coverage)

y_pred_ints

[29]:

| Coverage | ||

|---|---|---|

| 0.9 | ||

| lower | upper | |

| 1961-01 | 418.280122 | 464.281951 |

| 1961-02 | 402.215882 | 456.888054 |

| 1961-03 | 459.966115 | 522.110499 |

| 1961-04 | 442.589311 | 511.399213 |

| 1961-05 | 443.525029 | 518.409479 |

| 1961-06 | 506.585817 | 587.087736 |

| 1961-07 | 561.496771 | 647.248955 |

| 1961-08 | 557.363325 | 648.062362 |

| 1961-09 | 477.658059 | 573.047750 |

| 1961-10 | 407.915093 | 507.775353 |

| 1961-11 | 346.942927 | 451.082014 |

| 1961-12 | 394.708224 | 502.957139 |

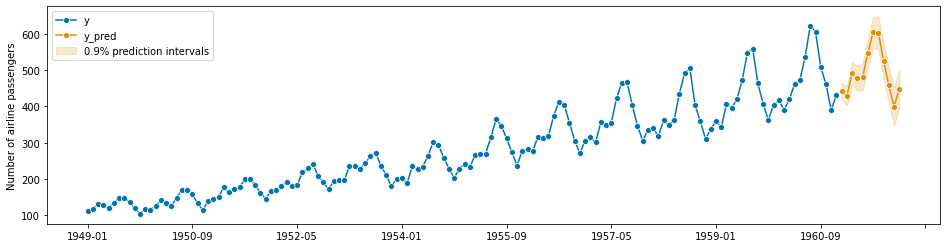

The return y_pred_ints is a pandas.DataFrame with a column multi-index: The first level is variable name from y in fit (or Coverage if no variable names were present), second level coverage fractions for which intervals were computed, in the same order as in input coverage; third level columns lower and upper. Rows are the indices for which forecasts were made (same as in y_pred or fh). Entries are lower/upper (as column name) bound of the nominal coverage

predictive interval for the index in the same row.

Pretty-plotting the predictive interval forecasts:

[30]:

from sktime.utils import plotting

# also requires predictions

y_pred = forecaster.predict()

fig, ax = plotting.plot_series(

y, y_pred, labels=["y", "y_pred"], pred_interval=y_pred_ints

)

predict_quantiles - quantile forecasts#

sktime offers predict_quantiles as a unified interface to return quantile values of predictions. Similar to predict_interval.

predict_quantiles has an argument alpha, containing the quantile values being queried. Similar to the case of the predict_interval, alpha can be a float, or a list of floats.

[31]:

y_pred_quantiles = forecaster.predict_quantiles(alpha=[0.275, 0.975])

y_pred_quantiles

[31]:

| Quantiles | ||

|---|---|---|

| 0.275 | 0.975 | |

| 1961-01 | 432.922220 | 468.688317 |

| 1961-02 | 419.617697 | 462.124924 |

| 1961-03 | 479.746288 | 528.063108 |

| 1961-04 | 464.491078 | 517.990290 |

| 1961-05 | 467.360287 | 525.582417 |

| 1961-06 | 532.209080 | 594.798752 |

| 1961-07 | 588.791161 | 655.462877 |

| 1961-08 | 586.232268 | 656.750127 |

| 1961-09 | 508.020008 | 582.184819 |

| 1961-10 | 439.699997 | 517.340642 |

| 1961-11 | 380.089755 | 461.057159 |

| 1961-12 | 429.163185 | 513.325951 |

y_pred_quantiles, the output of predict_quantiles, is a pandas.DataFrame with a two-level column multiindex. The first level is variable name from y in fit (or Quantiles if no variable names were present), second level are the quantile values (from alpha) for which quantile predictions were queried. Rows are the indices for which forecasts were made (same as in y_pred or fh). Entries are the quantile predictions for that variable, that quantile value, for the time

index in the same row.

Remark: for clarity: quantile and (symmetric) interval forecasts can be translated into each other as follows.

alpha < 0.5: The alpha-quantile prediction is equal to the lower bound of a predictive interval with coverage = (0.5 - alpha) * 2

alpha > 0.5: The alpha-quantile prediction is equal to the upper bound of a predictive interval with coverage = (alpha - 0.5) * 2

predict_var - variance predictions#

predict_var produces variance predictions:

[32]:

y_pred_var = forecaster.predict_var()

y_pred_var

[32]:

| 0 | |

|---|---|

| 1961-01 | 195.540039 |

| 1961-02 | 276.196489 |

| 1961-03 | 356.852939 |

| 1961-04 | 437.509389 |

| 1961-05 | 518.165839 |

| 1961-06 | 598.822289 |

| 1961-07 | 679.478739 |

| 1961-08 | 760.135189 |

| 1961-09 | 840.791639 |

| 1961-10 | 921.448089 |

| 1961-11 | 1002.104539 |

| 1961-12 | 1082.760989 |

The format of the output y_pred_var is the same as for predict, except that this is always coerced to a pandas.DataFrame, and entries are not point predictions but variance predictions.

predict_proba - distribution predictions#

To predict full predictive distributions, predict_proba can be used. As this returns tensorflow Distribution objects, the deep learning dependency set dl of sktime (which includes tensorflow and tensorflow-probability dependencies) must be installed.

[33]:

y_pred_proba = forecaster.predict_proba()

y_pred_proba

[33]:

<tfp.distributions.Normal 'Normal' batch_shape=[12, 1] event_shape=[] dtype=float32>

Distributions returned by predict_proba are by default marginal at time points, not joint over time points. More precisely, the returned Distribution object is formatted and to be interpreted as follows: * Batch shape is 1D and same length as fh * Event shape is 1D, with length equal to number of variables being forecast * i-th (batch) distribution is forecast for i-th entry of fh * j-th (event) component is j-th variable, same order as y in fit/update

To return joint forecast distributions, the marginal parameter can be set to False (currently work in progress). In this case, a Distribution with 2D event shape (len(fh), len(y)) is returned.

1.2.6 Panel forecasts and hierarchical forecasts#

sktime provides a unified interface to make panel and hierarchical forecasts.

All sktime forecasters can be applied to panel and hierarchical data, which needs to be presented in specific input formats. Forecasters that are not genuinely panel or hierarchical forecasters will be applied by instance.

The recommended (not the only) format to pass panel and hierarchical data is a pandas.DataFrame with MultiIndex row. In this MultiIndex, the last level must be in an sktime compatible time index format, the remaining levels are panel or hierarchy nodes.

Example data:

[34]:

from sktime.utils._testing.hierarchical import _bottom_hier_datagen

y = _bottom_hier_datagen(no_levels=2)

y

[34]:

| passengers | |||

|---|---|---|---|

| l2_agg | l1_agg | timepoints | |

| l2_node01 | l1_node04 | 1949-01 | 1751.046693 |

| 1949-02 | 1847.272729 | ||

| 1949-03 | 2072.660808 | ||

| 1949-04 | 2024.264252 | ||

| 1949-05 | 1895.470000 | ||

| ... | ... | ... | ... |

| l2_node03 | l1_node05 | 1960-08 | 7843.728855 |

| 1960-09 | 6557.204770 | ||

| 1960-10 | 5942.431795 | ||

| 1960-11 | 5016.687658 | ||

| 1960-12 | 5563.869028 |

864 rows × 1 columns

As stated, all forecasters, genuinely hierarchical or not, can be applied, with all workflows described in this section, to produce hierarchical forecasts.

The syntax is exactly the same as for plain time series, except for the hierarchy levels in input and output data:

[35]:

from sktime.forecasting.arima import ARIMA

fh = [1, 2, 3]

forecaster = ARIMA()

forecaster.fit(y, fh=fh)

forecaster.predict()

[35]:

| passengers | |||

|---|---|---|---|

| l2_agg | l1_agg | timepoints | |

| l2_node01 | l1_node04 | 1961-01 | 7025.301868 |

| 1961-02 | 6932.869186 | ||

| 1961-03 | 6843.846928 | ||

| l2_node02 | l1_node01 | 1961-01 | 426.544850 |

| 1961-02 | 421.282983 | ||

| 1961-03 | 416.207550 | ||

| l1_node02 | 1961-01 | 2831.238136 | |

| 1961-02 | 2796.463164 | ||

| 1961-03 | 2762.919857 | ||

| l1_node03 | 1961-01 | 3281.334598 | |

| 1961-02 | 3235.589398 | ||

| 1961-03 | 3191.591150 | ||

| l1_node06 | 1961-01 | 699.784723 | |

| 1961-02 | 687.976011 | ||

| 1961-03 | 676.678320 | ||

| l2_node03 | l1_node05 | 1961-01 | 5492.522368 |

| 1961-02 | 5423.732250 | ||

| 1961-03 | 5357.407064 |

Similar to multivariate forecasting, forecasters that are not genuinely hierarchical fit by instance. The forecasters fitted by instance can be accessed in the forecasters_ parameter, which is a pandas.DataFrame where forecasters for a given instance are placed in the row with the index of the instance for which they make forecasts:

[36]:

forecaster.forecasters_

[36]:

| forecasters | ||

|---|---|---|

| l2_agg | l1_agg | |

| l2_node01 | l1_node04 | ARIMA() |

| l2_node02 | l1_node01 | ARIMA() |

| l1_node02 | ARIMA() | |

| l1_node03 | ARIMA() | |

| l1_node06 | ARIMA() | |

| l2_node03 | l1_node05 | ARIMA() |

If the data is both hierarchical and multivariate, and the forecaster cannot genuinely deal with either, the forecasters_ attribute will have both column indices, for variables, and row indices, for instances, with forecasters fitted per instance and variable:

[37]:

from sktime.forecasting.arima import ARIMA

from sktime.utils._testing.hierarchical import _make_hierarchical

y = _make_hierarchical(n_columns=2)

fh = [1, 2, 3]

forecaster = ARIMA()

forecaster.fit(y, fh=fh)

forecaster.forecasters_

[37]:

| c0 | c1 | ||

|---|---|---|---|

| h0 | h1 | ||

| h0_0 | h1_0 | ARIMA() | ARIMA() |

| h1_1 | ARIMA() | ARIMA() | |

| h1_2 | ARIMA() | ARIMA() | |

| h1_3 | ARIMA() | ARIMA() | |

| h0_1 | h1_0 | ARIMA() | ARIMA() |

| h1_1 | ARIMA() | ARIMA() | |

| h1_2 | ARIMA() | ARIMA() | |

| h1_3 | ARIMA() | ARIMA() |

Further details on hierarchical forecasting, including reduction, aggregation, reconciliation, are presented in the “hierarchical forecasting” tutorial.

It is good practice to evaluate statistical performance of a forecaster before deploying it, and regularly re-evaluate performance if in continuous deployment. The evaluation workflow for the basic batch forecasting task, as solved by the workflow in Section 1.2, consists of comparing batch forecasts with actuals. This is sometimes called (batch-wise) backtesting.

The basic evaluation workflow is as follows:

Splitting a representatively chosen historical series into a temporal training and test set. The test set should be temporally in the future of the training set.

Obtaining batch forecasts, as in Section 1.2, by fitting a forecaster to the training set, and querying predictions for the test set

Specifying a quantitative performance metric to compare the actual test set against predictions

Computing the quantitative performance on the test set

Testing whether this performance is statistically better than a chosen baseline performance

NOTE: Step 5 (testing) is currently not supported in sktime, but is on the development roadmap. For the time being, it is advised to use custom implementations of appropriate methods (e.g., Diebold-Mariano test; stationary confidence intervals).

NOTE: Note that this evaluation set-up determines how well a given algorithm would have performed on past data. Results are only insofar representative as future performance can be assumed to mirror past performance. This can be argued under certain assumptions (e.g., stationarity), but will in general be false. Monitoring of forecasting performance is hence advised in case an algorithm is applied multiple times.

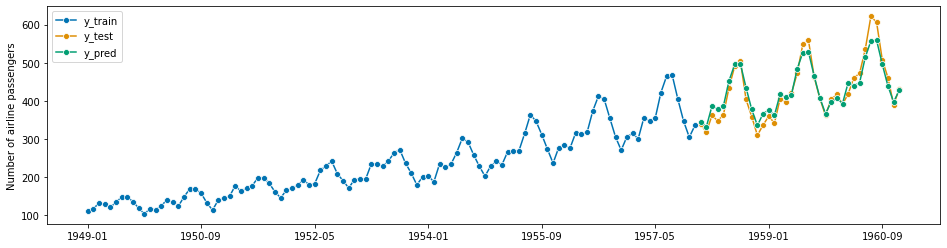

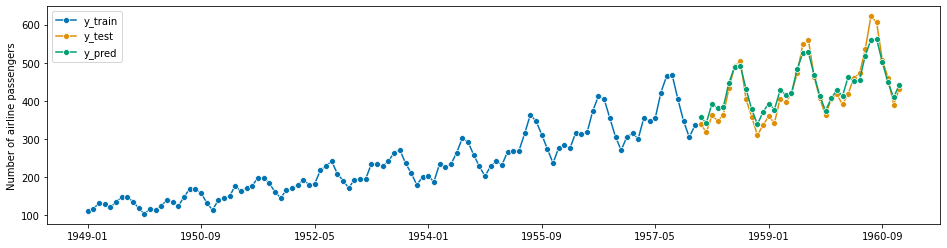

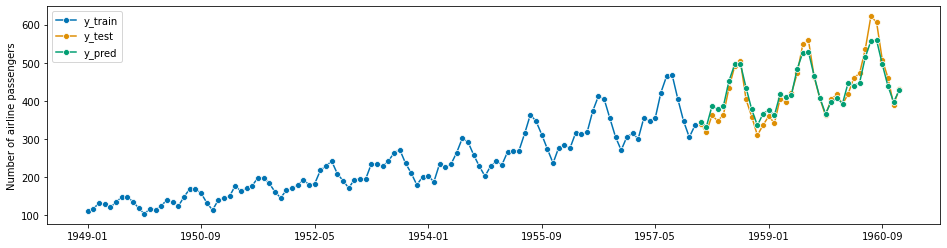

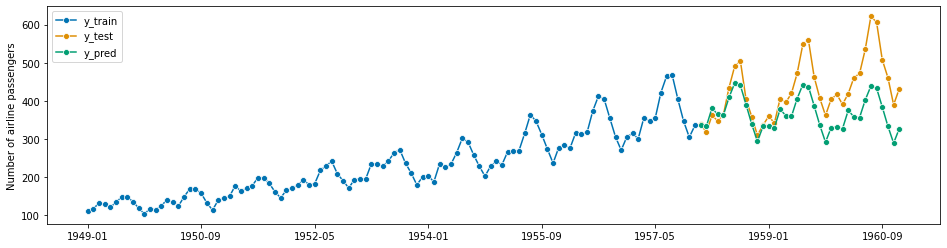

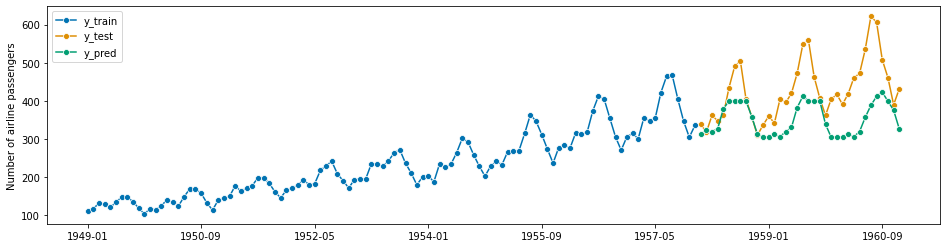

Example: In the example, we will us the same airline data as in Section 1.2. But, instead of predicting the next 3 years, we hold out the last 3 years of the airline data (below: y_test), and see how the forecaster would have performed three years ago, when asked to forecast the most recent 3 years (below: y_pred), from the years before (below: y_train). “how” is measured by a quantitative performance metric (below: mean_absolute_percentage_error). This is then considered as

an indication of how well the forecaster would perform in the coming 3 years (what was done in Section 1.2). This may or may not be a stretch depending on statistical assumptions and data properties (caution: it often is a stretch - past performance is in general not indicative of future performance).

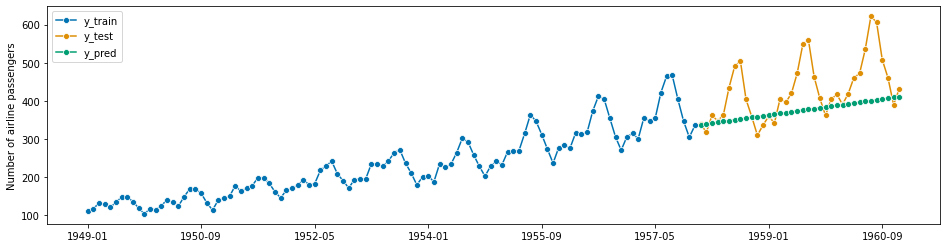

Step 1 - Splitting a historical data set in to a temporal train and test batch#

[38]:

from sktime.split import temporal_train_test_split

[39]:

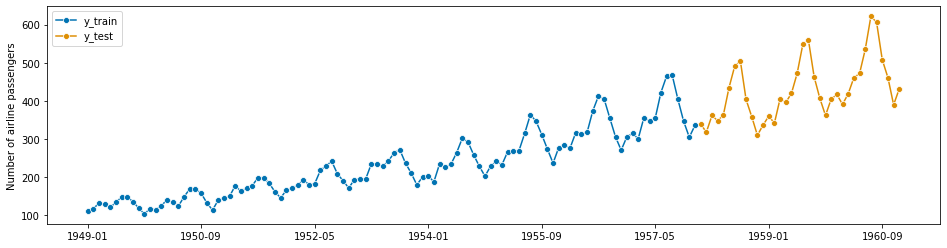

y = load_airline()

y_train, y_test = temporal_train_test_split(y, test_size=36)

# we will try to forecast y_test from y_train

[40]:

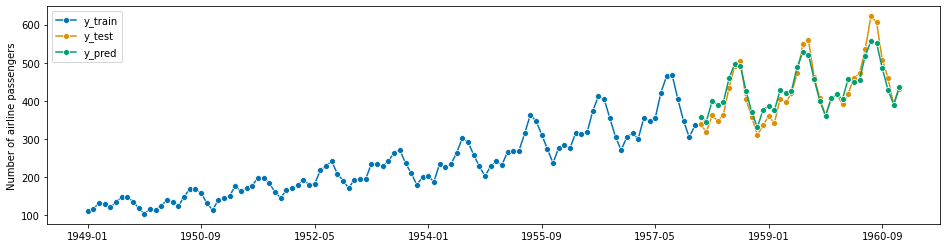

# plotting for illustration

plot_series(y_train, y_test, labels=["y_train", "y_test"])

print(y_train.shape[0], y_test.shape[0])

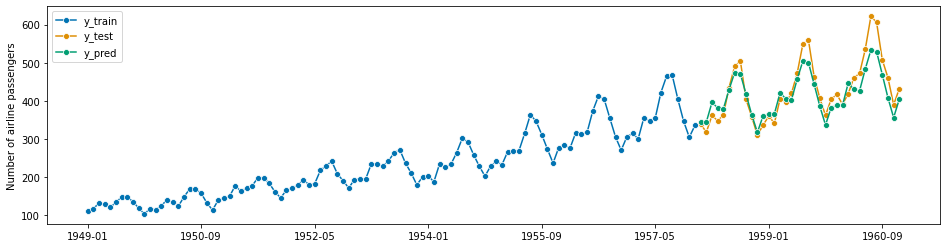

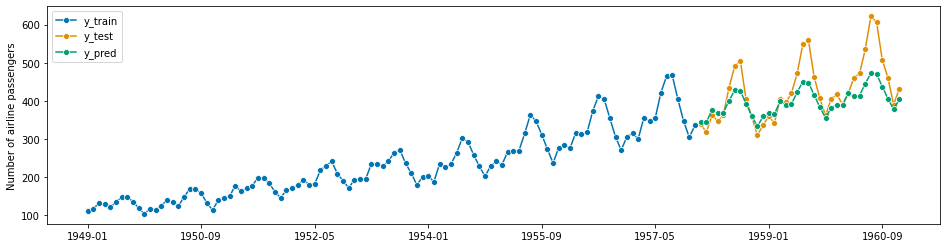

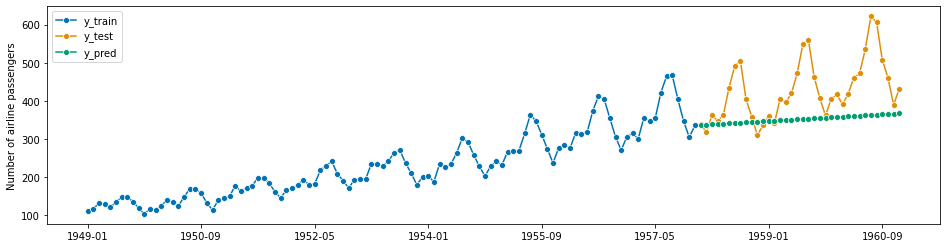

Step 2 - Making forecasts for y_test from y_train#

This is almost verbatim the workflow in Section 1.2, using y_train to predict the indices of y_test.

[41]:

# we can simply take the indices from `y_test` where they already are stored

fh = ForecastingHorizon(y_test.index, is_relative=False)

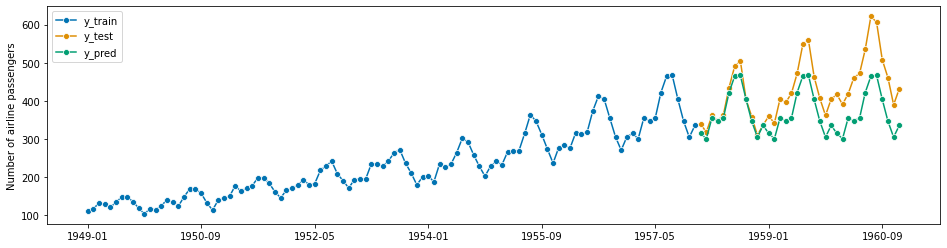

forecaster = NaiveForecaster(strategy="last", sp=12)

forecaster.fit(y_train)

# y_pred will contain the predictions

y_pred = forecaster.predict(fh)

[42]:

# plotting for illustration

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

[42]:

(<Figure size 1152x288 with 1 Axes>,

<AxesSubplot:ylabel='Number of airline passengers'>)

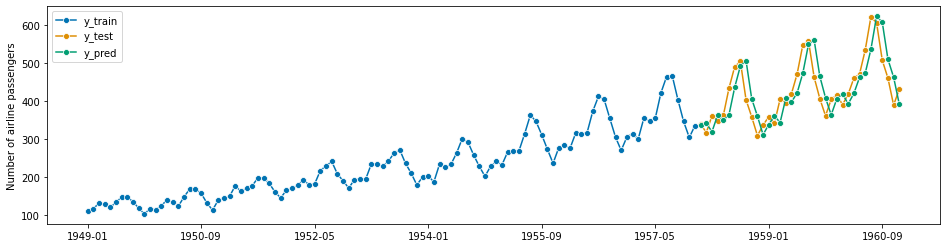

Steps 3 and 4 - Specifying a forecasting metric, evaluating on the test set#

The next step is to specify a forecasting metric. These are functions that return a number when input with prediction and actual series. They are different from sklearn metrics in that they accept series with indices rather than np.arrays. Forecasting metrics can be invoked in two ways:

using the lean function interface, e.g.,

mean_absolute_percentage_errorwhich is a python function(y_true : pd.Series, y_pred : pd.Series) -> floatusing the composable class interface, e.g.,

MeanAbsolutePercentageError, which is a python class, callable with the same signature

Casual users may opt to use the function interface. The class interface supports advanced use cases, such as parameter modification, custom metric composition, tuning over metric parameters (not covered in this tutorial)

[43]:

from sktime.performance_metrics.forecasting import mean_absolute_percentage_error

[44]:

# option 1: using the lean function interface

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

# note: the FIRST argument is the ground truth, the SECOND argument are the forecasts

# the order matters for most metrics in general

[44]:

0.13189432350948402

To properly interpret numbers like this, it is useful to understand properties of the metric in question (e.g., lower is better), and to compare against suitable baselines and contender algorithms (see step 5).

[45]:

from sktime.performance_metrics.forecasting import MeanAbsolutePercentageError

[46]:

# option 2: using the composable class interface

mape = MeanAbsolutePercentageError(symmetric=False)

# the class interface allows to easily construct variants of the MAPE

# e.g., the non-symmetric version

# it also allows for inspection of metric properties

# e.g., are higher values better (answer: no)?

mape.get_tag("lower_is_better")

[46]:

True

[47]:

# evaluation works exactly like in option 2, but with the instantiated object

mape(y_test, y_pred)

[47]:

0.13189432350948402

NOTE: Some metrics, such as mean_absolute_scaled_error, also require the training set for evaluation. In this case, the training set should be passed as a y_train argument. Refer to the API reference on individual metrics.

NOTE: The workflow is the same for forecasters that make use of exogeneous data - no X is passed to the metrics.

Step 5 - Testing performance against benchmarks#

In general, forecast performances should be quantitatively tested against benchmark performances.

Currently (sktime v0.12.x), this is a roadmap development item. Contributions are very welcome.

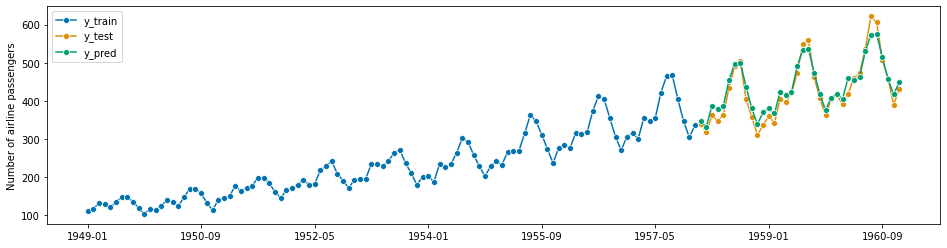

1.3.1 The basic batch forecast evaluation workflow in a nutshell - function metric interface#

For convenience, we present the basic batch forecast evaluation workflow in one cell. This cell is using the lean function metric interface.

[48]:

from sktime.datasets import load_airline

from sktime.forecasting.base import ForecastingHorizon

from sktime.forecasting.naive import NaiveForecaster

from sktime.performance_metrics.forecasting import mean_absolute_percentage_error

from sktime.split import temporal_train_test_split

[49]:

# step 1: splitting historical data

y = load_airline()

y_train, y_test = temporal_train_test_split(y, test_size=36)

# step 2: running the basic forecasting workflow

fh = ForecastingHorizon(y_test.index, is_relative=False)

forecaster = NaiveForecaster(strategy="last", sp=12)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

# step 3: specifying the evaluation metric and

# step 4: computing the forecast performance

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

# step 5: testing forecast performance against baseline

# under development

[49]:

0.13189432350948402

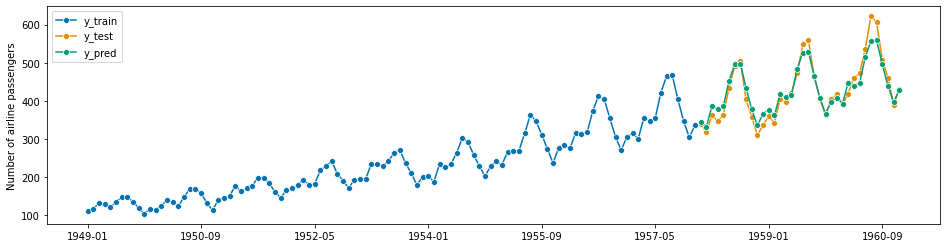

1.3.2 The basic batch forecast evaluation workflow in a nutshell - metric class interface#

For convenience, we present the basic batch forecast evaluation workflow in one cell. This cell is using the advanced class specification interface for metrics.

[50]:

from sktime.datasets import load_airline

from sktime.forecasting.base import ForecastingHorizon

from sktime.forecasting.naive import NaiveForecaster

from sktime.performance_metrics.forecasting import MeanAbsolutePercentageError

from sktime.split import temporal_train_test_split

[51]:

# step 1: splitting historical data

y = load_airline()

y_train, y_test = temporal_train_test_split(y, test_size=36)

# step 2: running the basic forecasting workflow

fh = ForecastingHorizon(y_test.index, is_relative=False)

forecaster = NaiveForecaster(strategy="last", sp=12)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

# step 3: specifying the evaluation metric

mape = MeanAbsolutePercentageError(symmetric=False)

# if function interface is used, just use the function directly in step 4

# step 4: computing the forecast performance

mape(y_test, y_pred)

# step 5: testing forecast performance against baseline

# under development

[51]:

0.13189432350948402

A common use case requires the forecaster to regularly update with new data and make forecasts on a rolling basis. This is especially useful if the same kind of forecast has to be made at regular time points, e.g., daily or weekly. sktime forecasters support this type of deployment workflow via the update and update_predict methods.

The update method can be called when a forecaster is already fitted, to ingest new data and make updated forecasts - this is referred to as an “update step”.

After the update, the forecaster’s internal “now” state (the cutoff) is set to the latest time stamp seen in the update batch (assumed to be later than previously seen data).

The general pattern is as follows:

Specify a forecasting strategy

Specify a relative forecasting horizon

Fit the forecaster to an initial batch of data using

fitMake forecasts for the relative forecasting horizon, using

predictObtain new data; use

updateto ingest new dataMake forecasts using

predictfor the updated dataRepeat 5 and 6 as often as required

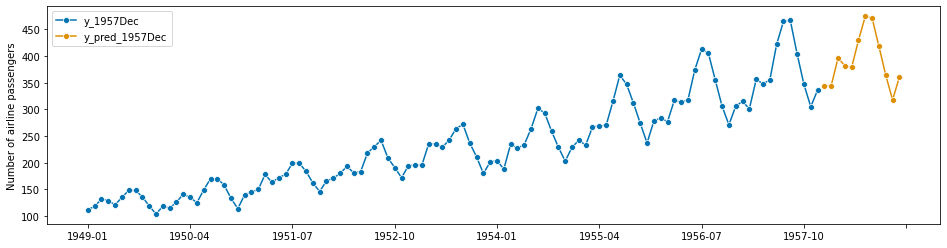

Example: suppose that, in the airline example, we want to make forecasts a year ahead, but every month, starting December 1957. The first few months, forecasts would be made as follows:

[52]:

from sktime.datasets import load_airline

from sktime.forecasting.ets import AutoETS

from sktime.utils.plotting import plot_series

[53]:

# we prepare the full data set for convenience

# note that in the scenario we will "know" only part of this at certain time points

y = load_airline()

[54]:

# December 1957

# this is the data known in December 1957

y_1957Dec = y[:-36]

# step 1: specifying the forecasting strategy

forecaster = AutoETS(auto=True, sp=12, n_jobs=-1)

# step 2: specifying the forecasting horizon: one year ahead, all months

fh = np.arange(1, 13)

# step 3: this is the first time we use the model, so we fit it

forecaster.fit(y_1957Dec)

# step 4: obtaining the first batch of forecasts for Jan 1958 - Dec 1958

y_pred_1957Dec = forecaster.predict(fh)

[55]:

# plotting predictions and past data

plot_series(y_1957Dec, y_pred_1957Dec, labels=["y_1957Dec", "y_pred_1957Dec"])

[55]:

(<Figure size 1152x288 with 1 Axes>,

<AxesSubplot:ylabel='Number of airline passengers'>)

[56]:

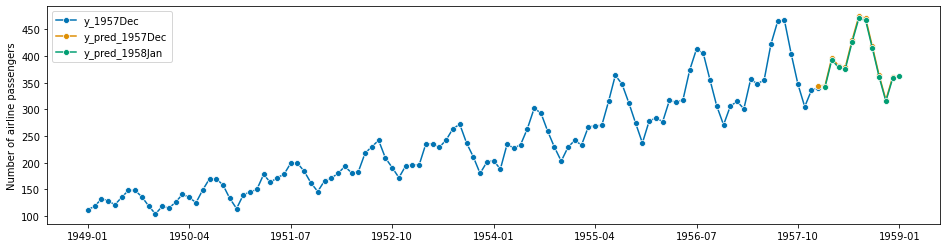

# January 1958

# new data is observed:

y_1958Jan = y[[-36]]

# step 5: we update the forecaster with the new data

forecaster.update(y_1958Jan)

# step 6: making forecasts with the updated data

y_pred_1958Jan = forecaster.predict(fh)

[57]:

# note that the fh is relative, so forecasts are automatically for 1 month later

# i.e., from Feb 1958 to Jan 1959

y_pred_1958Jan

[57]:

1958-02 341.514630

1958-03 392.849241

1958-04 378.518543

1958-05 375.658188

1958-06 426.006944

1958-07 470.569699

1958-08 467.100443

1958-09 414.450926

1958-10 360.957054

1958-11 315.202860

1958-12 357.898458

1959-01 363.036833

Freq: M, dtype: float64

[58]:

# plotting predictions and past data

plot_series(

y[:-35],

y_pred_1957Dec,

y_pred_1958Jan,

labels=["y_1957Dec", "y_pred_1957Dec", "y_pred_1958Jan"],

)

[58]:

(<Figure size 1152x288 with 1 Axes>,

<AxesSubplot:ylabel='Number of airline passengers'>)

[59]:

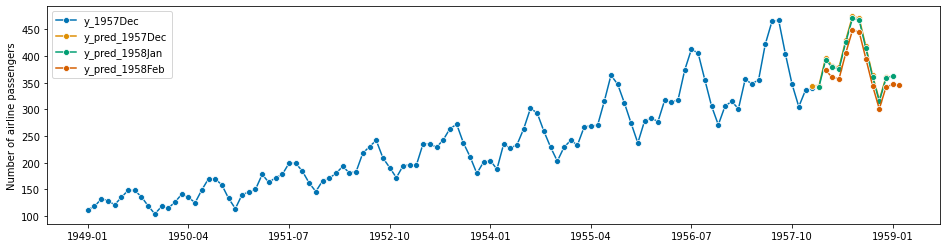

# February 1958

# new data is observed:

y_1958Feb = y[[-35]]

# step 5: we update the forecaster with the new data

forecaster.update(y_1958Feb)

# step 6: making forecasts with the updated data

y_pred_1958Feb = forecaster.predict(fh)

[60]:

# plotting predictions and past data

plot_series(

y[:-35],

y_pred_1957Dec,

y_pred_1958Jan,

y_pred_1958Feb,

labels=["y_1957Dec", "y_pred_1957Dec", "y_pred_1958Jan", "y_pred_1958Feb"],

)

[60]:

(<Figure size 1152x288 with 1 Axes>,

<AxesSubplot:ylabel='Number of airline passengers'>)

… and so on.

A shorthand for running first update and then predict is update_predict_single - for some algorithms, this may be more efficient than the separate calls to update and predict:

[61]:

# March 1958

# new data is observed:

y_1958Mar = y[[-34]]

# step 5&6: update/predict in one step

forecaster.update_predict_single(y_1958Mar, fh=fh)

[61]:

1958-04 349.161935

1958-05 346.920065

1958-06 394.051656

1958-07 435.839910

1958-08 433.316755

1958-09 384.841740

1958-10 335.535138

1958-11 293.171527

1958-12 333.275492

1959-01 338.595127

1959-02 336.983070

1959-03 388.121198

Freq: M, dtype: float64

In the rolling deployment mode, may be useful to move the estimator’s “now” state (the cutoff) to later, for example if no new data was observed, but time has progressed; or, if computations take too long, and forecasts have to be queried.

The update interface provides an option for this, via the update_params argument of update and other update functions.

If update_params is set to False, no model update computations are performed; only data is stored, and the internal “now” state (the cutoff) is set to the most recent date.

[62]:

# April 1958

# new data is observed:

y_1958Apr = y[[-33]]

# step 5: perform an update without re-computing the model parameters

forecaster.update(y_1958Apr, update_params=False)

[62]:

AutoETS(auto=True, n_jobs=-1, sp=12)

sktime can also simulate the update/predict deployment mode with a full batch of data.

This is not useful in deployment, as it requires all data to be available in advance; however, it is useful in playback, such as for simulations or model evaluation.

The update/predict playback mode can be called using update_predict and a re-sampling constructor which encodes the precise walk-forward scheme.

[63]:

# from sktime.datasets import load_airline

# from sktime.forecasting.ets import AutoETS

# from sktime.split import ExpandingWindowSplitter

# from sktime.utils.plotting import plot_series

NOTE: commented out - this part of the interface is currently undergoing a re-work. Contributions and PR are appreciated.

[64]:

# for playback, the full data needs to be loaded in advance

# y = load_airline()

[65]:

# step 1: specifying the forecasting strategy

# forecaster = AutoETS(auto=True, sp=12, n_jobs=-1)

# step 2: specifying the forecasting horizon

# fh - np.arange(1, 13)

# step 3: specifying the cross-validation scheme

# cv = ExpandingWindowSplitter()

# step 4: fitting the forecaster - fh should be passed here

# forecaster.fit(y[:-36], fh=fh)

# step 5: rollback

# y_preds = forecaster.update_predict(y, cv)

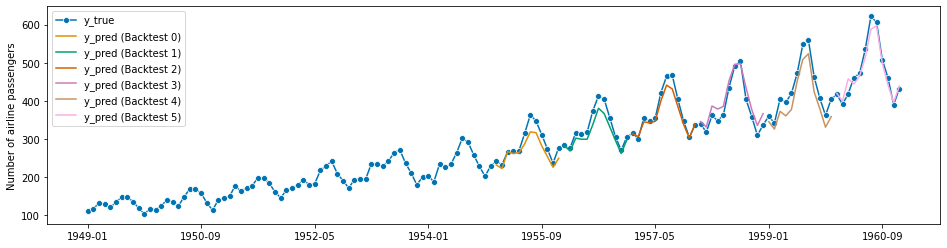

To evaluate forecasters with respect to their performance in rolling forecasting, the forecaster needs to be tested in a set-up mimicking rolling forecasting, usually on past data. Note that the batch back-testing as in Section 1.3 would not be an appropriate evaluation set-up for rolling deployment, as that tests only a single forecast batch.

The advanced evaluation workflow can be carried out using the evaluate benchmarking function. evaluate takes as arguments: - a forecaster to be evaluated - a scikit-learn re-sampling strategy for temporal splitting (cv below), e.g., ExpandingWindowSplitter or SlidingWindowSplitter - a strategy (string): whether the forecaster should be always be refitted or just fitted once and then updated

[66]:

from sktime.forecasting.arima import AutoARIMA

from sktime.forecasting.model_evaluation import evaluate

from sktime.split import ExpandingWindowSplitter

[67]:

forecaster = AutoARIMA(sp=12, suppress_warnings=True)

cv = ExpandingWindowSplitter(

step_length=12, fh=[1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12], initial_window=72

)

df = evaluate(forecaster=forecaster, y=y, cv=cv, strategy="refit", return_data=True)

df.iloc[:, :5]

[67]:

| test_MeanAbsolutePercentageError | fit_time | pred_time | len_train_window | cutoff | |

|---|---|---|---|---|---|

| 0 | 0.061710 | 4.026436 | 0.006171 | 72 | 1954-12 |

| 1 | 0.050042 | 5.211994 | 0.006386 | 84 | 1955-12 |

| 2 | 0.029802 | 8.024385 | 0.005885 | 96 | 1956-12 |

| 3 | 0.053773 | 4.231226 | 0.005654 | 108 | 1957-12 |

| 4 | 0.073820 | 5.250797 | 0.006525 | 120 | 1958-12 |

| 5 | 0.030976 | 11.651850 | 0.006294 | 132 | 1959-12 |

[68]:

# visualization of a forecaster evaluation

fig, ax = plot_series(

y,

df["y_pred"].iloc[0],

df["y_pred"].iloc[1],

df["y_pred"].iloc[2],

df["y_pred"].iloc[3],

df["y_pred"].iloc[4],

df["y_pred"].iloc[5],

markers=["o", "", "", "", "", "", ""],

labels=["y_true"] + ["y_pred (Backtest " + str(x) + ")" for x in range(6)],

)

ax.legend();

Todo: performance metrics, averages, and testing - contributions to sktime and the tutorial are welcome.

2. Forecasters in sktime - lookup, properties, main families#

This section summarizes how to:

search for forecasters in sktime

properties of forecasters, corresponding search options and tags

commonly used types of forecasters in

sktime

Generally, all forecasters available in sktime can be listed with the all_estimators command.

This will list all forecasters in sktime, even those whose soft dependencies are not installed.

[69]:

from sktime.registry import all_estimators

all_estimators("forecaster", as_dataframe=True)

[69]:

| name | estimator | |

|---|---|---|

| 0 | ARIMA | <class 'sktime.forecasting.arima.ARIMA'> |

| 1 | AutoARIMA | <class 'sktime.forecasting.arima.AutoARIMA'> |

| 2 | AutoETS | <class 'sktime.forecasting.ets.AutoETS'> |

| 3 | AutoEnsembleForecaster | <class 'sktime.forecasting.compose._ensemble.A... |

| 4 | BATS | <class 'sktime.forecasting.bats.BATS'> |

| 5 | BaggingForecaster | <class 'sktime.forecasting.compose._bagging.Ba... |

| 6 | ColumnEnsembleForecaster | <class 'sktime.forecasting.compose._column_ens... |

| 7 | ConformalIntervals | <class 'sktime.forecasting.conformal.Conformal... |

| 8 | Croston | <class 'sktime.forecasting.croston.Croston'> |

| 9 | DirRecTabularRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Dir... |

| 10 | DirRecTimeSeriesRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Dir... |

| 11 | DirectTabularRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Dir... |

| 12 | DirectTimeSeriesRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Dir... |

| 13 | DontUpdate | <class 'sktime.forecasting.stream._update.Dont... |

| 14 | DynamicFactor | <class 'sktime.forecasting.dynamic_factor.Dyna... |

| 15 | EnsembleForecaster | <class 'sktime.forecasting.compose._ensemble.E... |

| 16 | ExponentialSmoothing | <class 'sktime.forecasting.exp_smoothing.Expon... |

| 17 | ForecastX | <class 'sktime.forecasting.compose._pipeline.F... |

| 18 | ForecastingGridSearchCV | <class 'sktime.forecasting.model_selection._tu... |

| 19 | ForecastingPipeline | <class 'sktime.forecasting.compose._pipeline.F... |

| 20 | ForecastingRandomizedSearchCV | <class 'sktime.forecasting.model_selection._tu... |

| 21 | MultioutputTabularRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Mul... |

| 22 | MultioutputTimeSeriesRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Mul... |

| 23 | MultiplexForecaster | <class 'sktime.forecasting.compose._multiplexe... |

| 24 | NaiveForecaster | <class 'sktime.forecasting.naive.NaiveForecast... |

| 25 | NaiveVariance | <class 'sktime.forecasting.naive.NaiveVariance'> |

| 26 | OnlineEnsembleForecaster | <class 'sktime.forecasting.online_learning._on... |

| 27 | PolynomialTrendForecaster | <class 'sktime.forecasting.trend.PolynomialTre... |

| 28 | Prophet | <class 'sktime.forecasting.fbprophet.Prophet'> |

| 29 | ReconcilerForecaster | <class 'sktime.forecasting.reconcile.Reconcile... |

| 30 | RecursiveTabularRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Rec... |

| 31 | RecursiveTimeSeriesRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Rec... |

| 32 | SARIMAX | <class 'sktime.forecasting.sarimax.SARIMAX'> |

| 33 | STLForecaster | <class 'sktime.forecasting.trend.STLForecaster'> |

| 34 | StackingForecaster | <class 'sktime.forecasting.compose._stack.Stac... |

| 35 | StatsForecastAutoARIMA | <class 'sktime.forecasting.statsforecast.Stats... |

| 36 | TBATS | <class 'sktime.forecasting.tbats.TBATS'> |

| 37 | ThetaForecaster | <class 'sktime.forecasting.theta.ThetaForecast... |

| 38 | TransformedTargetForecaster | <class 'sktime.forecasting.compose._pipeline.T... |

| 39 | TrendForecaster | <class 'sktime.forecasting.trend.TrendForecast... |

| 40 | UnobservedComponents | <class 'sktime.forecasting.structural.Unobserv... |

| 41 | UpdateEvery | <class 'sktime.forecasting.stream._update.Upda... |

| 42 | UpdateRefitsEvery | <class 'sktime.forecasting.stream._update.Upda... |

| 43 | VAR | <class 'sktime.forecasting.var.VAR'> |

| 44 | VARMAX | <class 'sktime.forecasting.varmax.VARMAX'> |

| 45 | VECM | <class 'sktime.forecasting.vecm.VECM'> |

The entries of the last column of the resulting dataframe are classes which could be directly used for construction, or simply inspected for the correct import path.

For logic that loops over forecasters, the default output format may be more convenient:

[70]:

forecaster_list = all_estimators("forecaster", as_dataframe=False)

# this returns a list of (name, estimator) tuples

forecaster_list[0]

[70]:

('ARIMA', sktime.forecasting.arima.ARIMA)

All forecasters sktime have so-called tags which describe properties of the estimator, e.g., whether it is multivariate, probabilistic, or not. Use of tags, inspection, and retrieval will be described in this section.

Every forecaster has tags, which are key-value pairs that can describe capabilities or internal implementation details.

The most important “capability” style tags are the following:

requires-fh-in-fit - a boolean. Whether the forecaster requires the forecasting horizon fh already in fit (True), or whether it can be passed late in predict (False).

scitype:y - a string. Whether the forecaster is univariate ("univariate"), strictly multivariate ("multivariate"), or can deal with any number of variables ("both").

capability:pred_int - a boolean. Whether the forecaster can return probabilistic predictions via predict_interval etc, see Section 1.5.

ignores-exogeneous-X - a boolean. Whether the forecaster makes use of exogeneous variables X (False) or not (True). If the forecaster does not use X, it can still be passed for interface uniformity, and will be ignored.

handles-missing-data - a boolean. Whether the forecaster can deal with missing data in the inputs X or y.

Tags of a forecaster instance can be inspected via the get_tags (lists all tags) and get_tag (gets value for one tag) methods.

Tag values may depend on hyper-parameter choices.

[71]:

from sktime.forecasting.arima import ARIMA

ARIMA().get_tags()

[71]:

{'scitype:y': 'univariate',

'ignores-exogeneous-X': False,

'capability:pred_int': True,

'handles-missing-data': True,

'y_inner_mtype': 'pd.Series',

'X_inner_mtype': 'pd.DataFrame',

'requires-fh-in-fit': False,

'X-y-must-have-same-index': True,

'enforce_index_type': None,

'fit_is_empty': False,

'python_version': None,

'python_dependencies': 'pmdarima'}

The y_inner_mtype and X_inner_mtype indicate whether the forecaster can deal with panel or hierarchical data natively - if an panel or hierarchical mtype occurs here, it does (see data types tutorial).

An explanation for all tags can be obtained using the all_tags utility, see Section 2.2.3.

To list forecasters with their tags, the all_estimators utility can be used with its return_tags argument.

The resulting data frame can then be used for table queries or sub-setting.

[72]:

from sktime.registry import all_estimators

all_estimators(

"forecaster", as_dataframe=True, return_tags=["scitype:y", "requires-fh-in-fit"]

)

[72]:

| name | estimator | scitype:y | requires-fh-in-fit | |

|---|---|---|---|---|

| 0 | ARIMA | <class 'sktime.forecasting.arima.ARIMA'> | univariate | False |

| 1 | AutoARIMA | <class 'sktime.forecasting.arima.AutoARIMA'> | univariate | False |

| 2 | AutoETS | <class 'sktime.forecasting.ets.AutoETS'> | univariate | False |

| 3 | AutoEnsembleForecaster | <class 'sktime.forecasting.compose._ensemble.A... | univariate | False |

| 4 | BATS | <class 'sktime.forecasting.bats.BATS'> | univariate | False |

| 5 | BaggingForecaster | <class 'sktime.forecasting.compose._bagging.Ba... | univariate | False |

| 6 | ColumnEnsembleForecaster | <class 'sktime.forecasting.compose._column_ens... | both | False |

| 7 | ConformalIntervals | <class 'sktime.forecasting.conformal.Conformal... | univariate | False |

| 8 | Croston | <class 'sktime.forecasting.croston.Croston'> | univariate | False |

| 9 | DirRecTabularRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Dir... | univariate | True |

| 10 | DirRecTimeSeriesRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Dir... | univariate | True |

| 11 | DirectTabularRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Dir... | univariate | True |

| 12 | DirectTimeSeriesRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Dir... | univariate | True |

| 13 | DontUpdate | <class 'sktime.forecasting.stream._update.Dont... | univariate | False |

| 14 | DynamicFactor | <class 'sktime.forecasting.dynamic_factor.Dyna... | multivariate | False |

| 15 | EnsembleForecaster | <class 'sktime.forecasting.compose._ensemble.E... | univariate | False |

| 16 | ExponentialSmoothing | <class 'sktime.forecasting.exp_smoothing.Expon... | univariate | False |

| 17 | ForecastX | <class 'sktime.forecasting.compose._pipeline.F... | univariate | True |

| 18 | ForecastingGridSearchCV | <class 'sktime.forecasting.model_selection._tu... | both | False |

| 19 | ForecastingPipeline | <class 'sktime.forecasting.compose._pipeline.F... | both | False |

| 20 | ForecastingRandomizedSearchCV | <class 'sktime.forecasting.model_selection._tu... | both | False |

| 21 | MultioutputTabularRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Mul... | univariate | True |

| 22 | MultioutputTimeSeriesRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Mul... | univariate | True |

| 23 | MultiplexForecaster | <class 'sktime.forecasting.compose._multiplexe... | both | False |

| 24 | NaiveForecaster | <class 'sktime.forecasting.naive.NaiveForecast... | univariate | False |

| 25 | NaiveVariance | <class 'sktime.forecasting.naive.NaiveVariance'> | univariate | False |

| 26 | OnlineEnsembleForecaster | <class 'sktime.forecasting.online_learning._on... | univariate | False |

| 27 | PolynomialTrendForecaster | <class 'sktime.forecasting.trend.PolynomialTre... | univariate | False |

| 28 | Prophet | <class 'sktime.forecasting.fbprophet.Prophet'> | univariate | False |

| 29 | ReconcilerForecaster | <class 'sktime.forecasting.reconcile.Reconcile... | univariate | False |

| 30 | RecursiveTabularRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Rec... | univariate | False |

| 31 | RecursiveTimeSeriesRegressionForecaster | <class 'sktime.forecasting.compose._reduce.Rec... | univariate | False |

| 32 | SARIMAX | <class 'sktime.forecasting.sarimax.SARIMAX'> | univariate | False |

| 33 | STLForecaster | <class 'sktime.forecasting.trend.STLForecaster'> | univariate | False |

| 34 | StackingForecaster | <class 'sktime.forecasting.compose._stack.Stac... | univariate | True |

| 35 | StatsForecastAutoARIMA | <class 'sktime.forecasting.statsforecast.Stats... | univariate | False |

| 36 | TBATS | <class 'sktime.forecasting.tbats.TBATS'> | univariate | False |

| 37 | ThetaForecaster | <class 'sktime.forecasting.theta.ThetaForecast... | univariate | False |

| 38 | TransformedTargetForecaster | <class 'sktime.forecasting.compose._pipeline.T... | both | False |

| 39 | TrendForecaster | <class 'sktime.forecasting.trend.TrendForecast... | univariate | False |

| 40 | UnobservedComponents | <class 'sktime.forecasting.structural.Unobserv... | univariate | False |

| 41 | UpdateEvery | <class 'sktime.forecasting.stream._update.Upda... | univariate | False |

| 42 | UpdateRefitsEvery | <class 'sktime.forecasting.stream._update.Upda... | univariate | False |

| 43 | VAR | <class 'sktime.forecasting.var.VAR'> | multivariate | False |

| 44 | VARMAX | <class 'sktime.forecasting.varmax.VARMAX'> | multivariate | False |

| 45 | VECM | <class 'sktime.forecasting.vecm.VECM'> | multivariate | False |

To filter beforehand on certain tags and tag values, the filter_tags argument can be used:

[73]:

# this lists all forecasters that can deal with multivariate data

all_estimators(

"forecaster", as_dataframe=True, filter_tags={"scitype:y": ["multivariate", "both"]}

)

[73]:

| name | estimator | |

|---|---|---|

| 0 | ColumnEnsembleForecaster | <class 'sktime.forecasting.compose._column_ens... |

| 1 | DynamicFactor | <class 'sktime.forecasting.dynamic_factor.Dyna... |

| 2 | ForecastingGridSearchCV | <class 'sktime.forecasting.model_selection._tu... |

| 3 | ForecastingPipeline | <class 'sktime.forecasting.compose._pipeline.F... |

| 4 | ForecastingRandomizedSearchCV | <class 'sktime.forecasting.model_selection._tu... |

| 5 | MultiplexForecaster | <class 'sktime.forecasting.compose._multiplexe... |

| 6 | TransformedTargetForecaster | <class 'sktime.forecasting.compose._pipeline.T... |

| 7 | VAR | <class 'sktime.forecasting.var.VAR'> |

| 8 | VARMAX | <class 'sktime.forecasting.varmax.VARMAX'> |

| 9 | VECM | <class 'sktime.forecasting.vecm.VECM'> |

Important note: as said above, tag values can depend on hyper-parameter settings, e.g., a ForecastingPipeline can handle multivariate data only if the forecaster in it can handle multivariate data.

In retrieval as above, the tags for a class are usually set to indicate the most general potential value, e.g., if for some parameter choice the estimator can handle multivariate, it will appear on the list.

To list all forecaster tags with an explanation of the tag, the all_tags utility can be used:

[74]:

import pandas as pd

from sktime.registry import all_tags

# wrapping this in a pandas DataFrame for pretty display

pd.DataFrame(all_tags(estimator_types="forecaster"))[[0, 3]]

[74]:

| 0 | 3 | |

|---|---|---|

| 0 | X-y-must-have-same-index | do X/y in fit/update and X/fh in predict have ... |

| 1 | X_inner_mtype | which machine type(s) is the internal _fit/_pr... |

| 2 | capability:pred_int | does the forecaster implement predict_interval... |

| 3 | capability:pred_var | does the forecaster implement predict_variance? |

| 4 | enforce_index_type | passed to input checks, input conversion index... |

| 5 | ignores-exogeneous-X | does forecaster ignore exogeneous data (X)? |

| 6 | requires-fh-in-fit | does forecaster require fh passed already in f... |

| 7 | scitype:y | which series type does the forecaster support?... |

| 8 | y_inner_mtype | which machine type(s) is the internal _fit/_pr... |

sktime supports a number of commonly used forecasters, many of them interfaced from state-of-art forecasting packages. All forecasters are available under the unified sktime interface.

Some classes that are currently stably supported are:

ExponentialSmoothing,ThetaForecaster, andautoETSfromstatsmodelsARIMAandAutoARIMAfrompmdarimaAutoARIMAfromstatsforecastBATSandTBATSfromtbatsPolynomialTrendfor forecasting polynomial trendsProphetwhich interfaces Facebookprophet

This is not the full list, use all_estimators as demonstrated in Sections 2.1 and 2.2 for that.

For illustration, all estimators below will be presented on the basic forecasting workflow - though they also support the advanced forecasting and evaluation workflows under the unified sktime interface (see Section 1).

For use in the other workflows, simply replace the “forecaster specification block” (”forecaster=”) by the forecaster specification block in the examples presented below.

[75]:

# imports necessary for this chapter

from sktime.datasets import load_airline

from sktime.forecasting.base import ForecastingHorizon

from sktime.performance_metrics.forecasting import mean_absolute_percentage_error

from sktime.split import temporal_train_test_split

from sktime.utils.plotting import plot_series

# data loading for illustration (see section 1 for explanation)

y = load_airline()

y_train, y_test = temporal_train_test_split(y, test_size=36)

fh = ForecastingHorizon(y_test.index, is_relative=False)

sktime interfaces a number of statistical forecasting algorithms from statsmodels: exponential smoothing, theta, and auto-ETS.

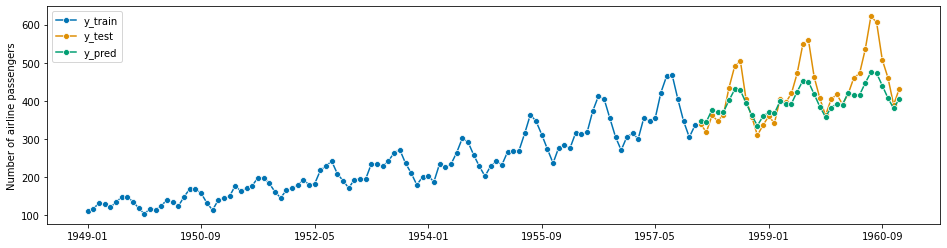

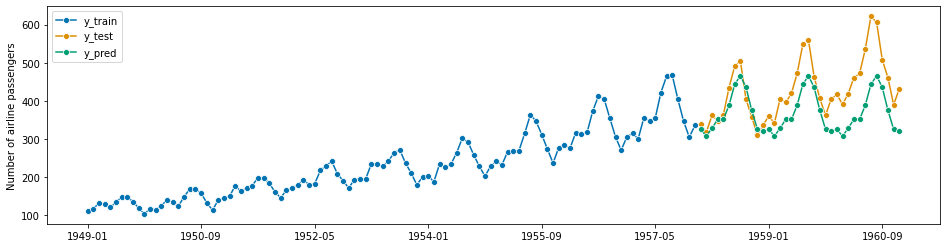

For example, to use exponential smoothing with an additive trend component and multiplicative seasonality on the airline data set, we can write the following. Note that since this is monthly data, a good choic for seasonal periodicity (sp) is 12 (= hypothesized periodicity of a year).

[76]:

from sktime.forecasting.exp_smoothing import ExponentialSmoothing

[77]:

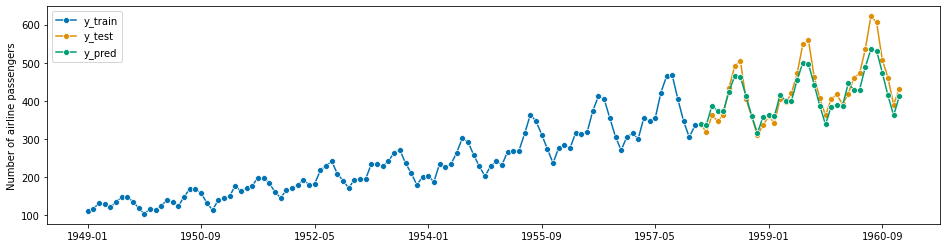

forecaster = ExponentialSmoothing(trend="add", seasonal="additive", sp=12)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

[77]:

0.05114163237371178

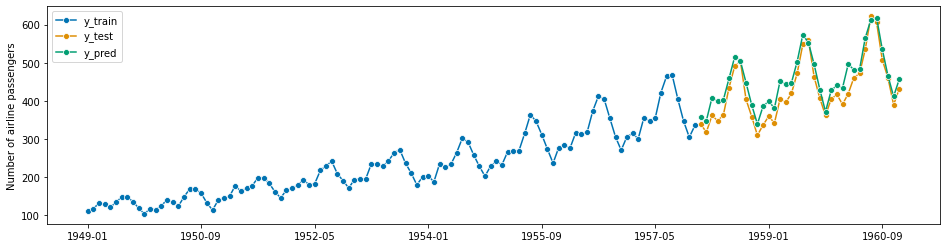

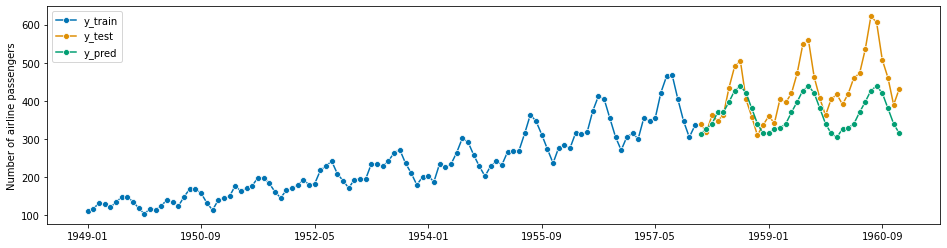

The exponential smoothing of state space model can also be automated similar to the ets function in R. This is implemented in the AutoETS forecaster.

[78]:

from sktime.forecasting.ets import AutoETS

[79]:

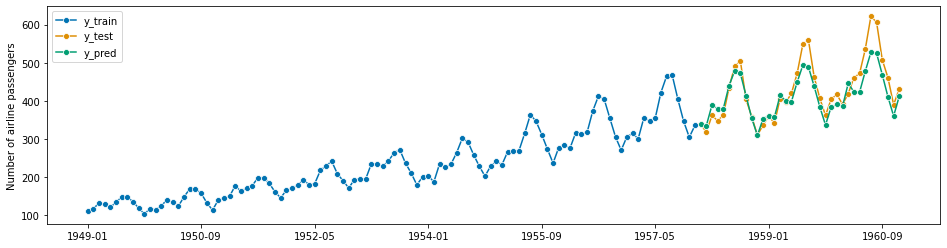

forecaster = AutoETS(auto=True, sp=12, n_jobs=-1)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

[79]:

0.06186318537056982

[80]:

# todo: explain Theta; explain how to get theta-lines

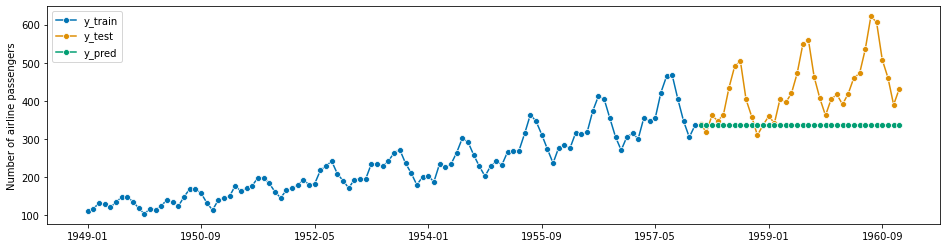

sktime interfaces pmdarima for its ARIMA class models. For a classical ARIMA model with set parameters, use the ARIMA forecaster:

[81]:

from sktime.forecasting.arima import ARIMA

[82]:

forecaster = ARIMA(

order=(1, 1, 0), seasonal_order=(0, 1, 0, 12), suppress_warnings=True

)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

[82]:

0.04356744885278522

AutoARIMA is an automatically tuned ARIMA variant that obtains the optimal pdq parameters automatically:

[83]:

from sktime.forecasting.arima import AutoARIMA

[84]:

forecaster = AutoARIMA(sp=12, suppress_warnings=True)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

[84]:

0.041489714388809135

[85]:

forecaster = AutoARIMA(sp=12, suppress_warnings=True)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_pred, y_test)

[85]:

0.040936759322166255

[86]:

# to obtain the fitted parameters, run

forecaster.get_fitted_params()

# should these not include pdq?

[86]:

{'ar.L1': -0.24111779230017605,

'sigma2': 92.74986650446229,

'order': (1, 1, 0),

'seasonal_order': (0, 1, 0, 12),

'aic': 704.0011679023331,

'aicc': 704.1316026849419,

'bic': 709.1089216855343,

'hqic': 706.0650836393346}

sktime interfaces BATS and TBATS from the `tbats <intive-DataScience/tbats>`__ package.

[87]:

from sktime.forecasting.bats import BATS

[88]:

forecaster = BATS(sp=12, use_trend=True, use_box_cox=False)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

[88]:

0.08185558959286515

[89]:

from sktime.forecasting.tbats import TBATS

[90]:

forecaster = TBATS(sp=12, use_trend=True, use_box_cox=False)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

[90]:

0.08024090844021753

sktime provides an interface to `fbprophet <facebook/prophet>`__ by Facebook.

[91]:

from sktime.forecasting.fbprophet import Prophet

The current interface does not support period indices, only pd.DatetimeIndex. Consider improving this by contributing the sktime.

[92]:

# Convert index to pd.DatetimeIndex

z = y.copy()

z = z.to_timestamp(freq="M")

z_train, z_test = temporal_train_test_split(z, test_size=36)

[93]:

forecaster = Prophet(

seasonality_mode="multiplicative",

n_changepoints=int(len(y_train) / 12),

add_country_holidays={"country_name": "Germany"},

yearly_seasonality=True,

weekly_seasonality=False,

daily_seasonality=False,

)

forecaster.fit(z_train)

y_pred = forecaster.predict(fh.to_relative(cutoff=y_train.index[-1]))

y_pred.index = y_test.index

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

[93]:

0.07276862950407971

We can also use the `UnobservedComponents <https://www.statsmodels.org/stable/generated/statsmodels.tsa.statespace.structural.UnobservedComponents.html>`__ class from `statsmodels <https://www.statsmodels.org/stable/index.html>`__ to generate predictions using a state space model.

[94]:

from sktime.forecasting.structural import UnobservedComponents

[95]:

# We can model seasonality using Fourier modes as in the Prophet model.

forecaster = UnobservedComponents(

level="local linear trend", freq_seasonal=[{"period": 12, "harmonics": 10}]

)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

[95]:

0.0497366365924174

sktime interfaces StatsForecast for its AutoARIMA class models. AutoARIMA is an automatically tuned ARIMA variant that obtains the optimal pdq parameters automatically:

[96]:

from sktime.forecasting.statsforecast import StatsForecastAutoARIMA

[97]:

forecaster = StatsForecastAutoARIMA(sp=12)

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_pred, y_test)

[97]:

0.04093539044441262

3. Advanced composition patterns - pipelines, reduction, autoML, and more#

sktime supports a number of advanced composition patterns to create forecasters out of simpler components:

Reduction - building a forecaster from estimators of “simpler” scientific types, like

scikit-learnregressors. A common example is feature/label tabulation by rolling window, aka the “direct reduction strategy”.Tuning - determining values for hyper-parameters of a forecaster in a data-driven manner. A common example is grid search on temporally rolling re-sampling of train/test splits.

Pipelining - concatenating transformers with a forecaster to obtain one forecaster. A common example is detrending and deseasonalizing then forecasting, an instance of this is the common “STL forecaster”.

AutoML, also known as automated model selection - using automated tuning strategies to select not only hyper-parameters but entire forecasting strategies. A common example is on-line multiplexer tuning.

For illustration, all estimators below will be presented on the basic forecasting workflow - though they also support the advanced forecasting and evaluation workflows under the unified sktime interface (see Section 1).

For use in the other workflows, simply replace the “forecaster specification block” (”forecaster=”) by the forecaster specification block in the examples presented below.

[98]:

# imports necessary for this chapter

from sktime.datasets import load_airline

from sktime.forecasting.base import ForecastingHorizon

from sktime.performance_metrics.forecasting import mean_absolute_percentage_error

from sktime.split import temporal_train_test_split

from sktime.utils.plotting import plot_series

# data loading for illustration (see section 1 for explanation)

y = load_airline()

y_train, y_test = temporal_train_test_split(y, test_size=36)

fh = ForecastingHorizon(y_test.index, is_relative=False)

sktime provides a meta-estimator that allows the use of any scikit-learn estimator for forecasting.

modular and compatible with scikit-learn, so that we can easily apply any scikit-learn regressor to solve our forecasting problem,

parametric and tuneable, allowing us to tune hyper-parameters such as the window length or strategy to generate forecasts

adaptive, in the sense that it adapts the scikit-learn’s estimator interface to that of a forecaster, making sure that we can tune and properly evaluate our model

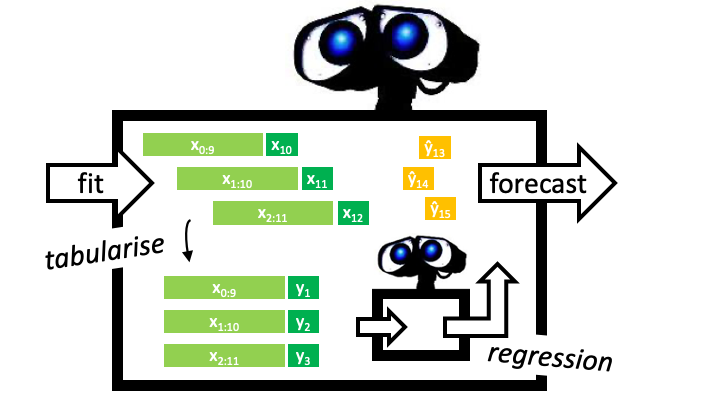

Example: we will define a tabulation reduction strategy to convert a k-nearest neighbors regressor (sklearn KNeighborsRegressor) into a forecaster. The composite algorithm is an object compliant with the sktime forecaster interface (picture: big robot), and contains the regressor as a parameter accessible component (picture: little robot). In fit, the composite algorithm uses a sliding window strategy to tabulate the data, and fit the regressor to the tabulated data (picture:

left half). In predict, the composite algorithm presents the regressor with the last observed window to obtain predictions (picture: right half).

Below, the composite is constructed using the shorthand function make_reduction which produces a sktime estimator of forecaster scitype. It is called with a constructed scikit-learn regressor, regressor, and additional parameter which can be later tuned as hyper-parameters

[99]:

from sklearn.neighbors import KNeighborsRegressor

from sktime.forecasting.compose import make_reduction

[100]:

regressor = KNeighborsRegressor(n_neighbors=1)

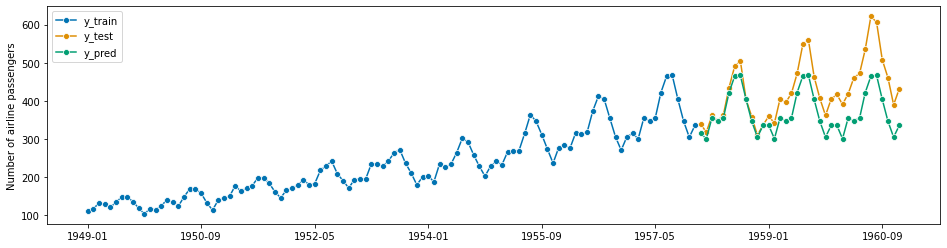

forecaster = make_reduction(regressor, window_length=15, strategy="recursive")

[101]:

forecaster.fit(y_train)

y_pred = forecaster.predict(fh)

plot_series(y_train, y_test, y_pred, labels=["y_train", "y_test", "y_pred"])

mean_absolute_percentage_error(y_test, y_pred, symmetric=False)

[101]:

0.12887507224382988

In the above example we use the “recursive” reduction strategy. Other implemented strategies are: * “direct”, * “dirrec”, * “multioutput”.

Parameters can be inspected using scikit-learn compatible get_params functionality (and set using set_params). This provides tunable and nested access to parameters of the KNeighborsRegressor (as estimator_etc), and the window_length of the reduction strategy. Note that the strategy is not accessible, as underneath the utility function this is mapped on separate algorithm classes. For tuning over algorithms, see the “autoML” section below.

[102]:

forecaster.get_params()

[102]:

{'estimator__algorithm': 'auto',

'estimator__leaf_size': 30,

'estimator__metric': 'minkowski',

'estimator__metric_params': None,

'estimator__n_jobs': None,

'estimator__n_neighbors': 1,